- An era of sustained positive real interest rates should prove beneficial for bond investors.

- The sharp rise in interest rates means bond yields have grown markedly over the past two years; over time, these higher yields should eventually provide higher total returns to investors than before the rate rises.

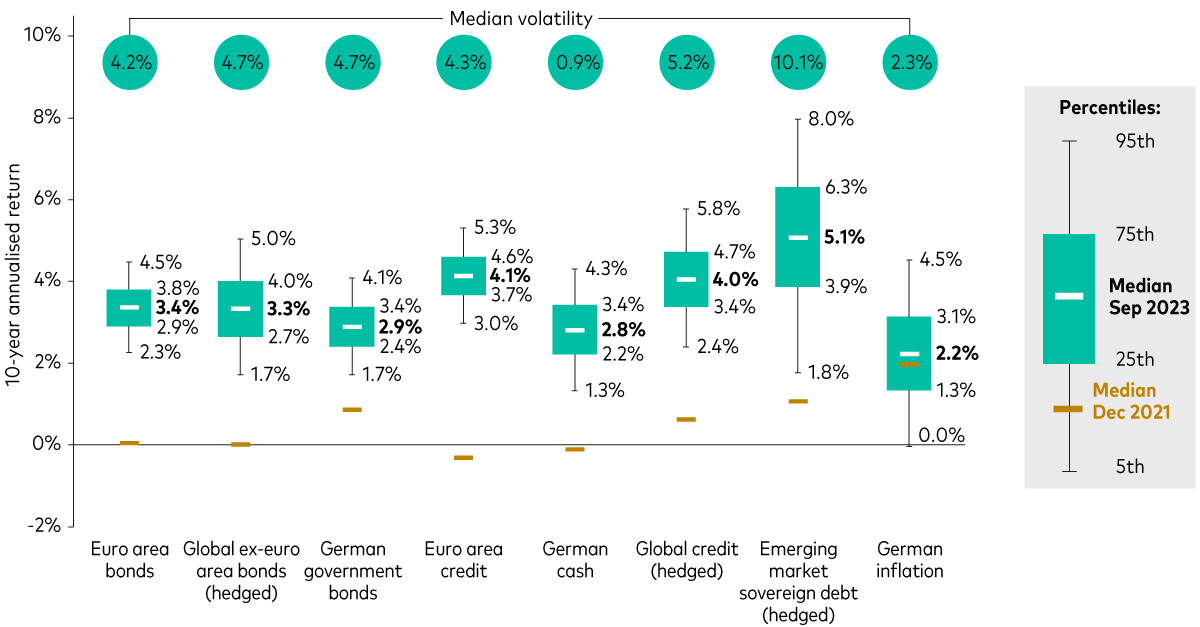

- Over the next decade, we expect euro and global ex-euro (EUR hedged) bonds to return around 3.4% and 3.3%, respectively, on an annualised basis.

In our Vanguard Economic and Market Outlook for 2024: A Return To Sound Money, one of the key themes we explore is how the persistence of positive real interest rates will impact fixed income returns in investor portfolios.

Short term pain can lead to long-term gain. Nowhere has that pain been felt more over the last two years than in bond markets, where sharp rises in interest rates have led to a signficant repricing of existing bonds – and painful losses for bond investors.

Yet while the impact of interest rate increases can be felt immediately, the longer-term benefits of higher rates take time to play out. It may not seem like it now, but a higher rate environment should ultimately prove beneficial for bond investors, providing signficant additional value through higher returns and higher levels of income that, if reinvested, should eventually more than offset the previous capital losses from the past two years. Looking ahead, our outlook for long-term bond returns has increased to levels not seen since the decade before the global financial crisis of 2008, when yields were last above 4%1.

Short-term pain for long-term gains

While we expect major central banks to start cutting policy rates from around the middle of next year, we expect short- and long-term rates to settle at higher levels than we became used to in the previous decade. The structural shift towards an era of positive real rates – an era of sound money - will have profound implications for the global economy and financial markets, and is good news for bond investors.

To illustrate why, the chart below shows the hypothetical performance of a lump sum invested in a portfolio of bonds at the end of May 20212. The dark green line highlights the impact of interest rate increases on the value of the portfolio, with the brown line showing the hypothetical expected growth over the next ten years in the new higher rate environment. The green line shows the hypothetical performance of the same portfolio if rates had remained low.

As we have witnessed over the last two years, the sharp rate rises initially caused the bond portfolio to decline in value, resulting in significant losses throughout 2022. Yet, as bond yields have increased to their current levels, we can see that, over time, the portfolio recovers in value. The improved return outlook helps replenish the previous capital losses (brown line), eventually providing higher cumulative bond returns to investors than they would have earned if rates had not increased in the first place (green line).

Rising rates mean higher returns for long-term investors

Past performance is not a reliable indicator of future results. Any projections should be regarded as hypothetical in nature and do not reflect or guarantee future results.

Notes: The chart shows actual returns for the Bloomberg Global Aggregate Bond Index Euro Hedged along with Vanguard’s forecast for cumulative returns over the subsequent 10 years, as at 31 December 2021 and 30 September 2023. The dotted lines represent the 10th and 90th percentiles of the forecasted distribution.

Source: Vanguard calculations, based on data from Bloomberg, as at 30 September 2023.

Important: The projections and other information generated by the VCMM regarding the likelihood of various investment outcomes are hypothetical in nature, do not reflect actual investment results and are not guarantees of future results. Results from the model may vary with each use and over time.

A return to sound money

Today, thanks to the significant increases in rates, the income portion of bond returns has grown markedly – which we expect will not only boost total long-term bond returns but also marks a shift in the contribution of bond income to total portfolio returns.

According to our latest forecasts, we now expect euro area and global ex-euro area (euro hedged) bonds to return around 3.4% and 3.3%, respectively, on an annualised basis over the next decade, compared with our previous 10-year annualised forecasts of 0% and 0%, respectively, before the rate-hiking cycle began. Importantly, we expect global bond returns to rival those of global equities, which we believe will deliver a median annualised total return of around 4.5% over the same time period, but with a higher level of volatility than global bonds3.

Expected 10-year annualised asset class returns for euro area investors

Notes: The forecast corresponds to the distribution of 10,000 VCMM simulations for 10-year annualised nominal returns in euros for the asset classes highlighted here. The median 10-year annualised nominal return forecasts as at the end of September 2023 are shown by the white lines and as at the end of December 2021 are shown by the gold lines. Median volatility is the 50th percentile of an assets class's distribution of annualised standard deviation of returns. Asset-class returns do not take into account management fees and expenses, nor do they reflect the effect of taxes. Returns do reflect the reinvestment of income and capital gains. Indices are unmanaged; therefore, direct investment is not possible. Benchmarks used for asset classes: Euro area bonds: Bloomberg Euro-Aggregate Bond Index; Global ex-euro area bonds (hedged): Bloomberg Global Aggregate ex-Euro Bond Index Euro Hedged; German government bonds: Bloomberg Germany Treasury Bond Index; Euro area credit: Bloomberg Euro-Aggregate - Credit Bond Index; German cash: German 3-month sovereign yield; Global credit (hedged): Bloomberg Global Aggregate - Corporates Bond Index Euro Hedged; Emerging market sovereign debt: Bloomberg Emerging Markets USD Sovereign Bond Index - 10% Country Capped Euro Hedged; German inflation: Consumer Price Index.

Source: Vanguard calculations in euros, as at 30 September 2023.

IMPORTANT: The projections and other information generated by the VCMM regarding the likelihood of various investment outcomes are hypothetical in nature, do not reflect actual investment results and are not guarantees of future results. Results from the model may vary with each use and over time.

Past performance is no guarantee of future returns. The performance of an index is not an exact representation of any particular investment, as you cannot invest directly in an index.

A bumpy transition

This doesn’t mean volatility is behind us. Markets are eagerly anticipating rate cuts by central banks in 2024. A fall in rates will push up the price of existing bonds, which will benefit bond investors – but it’s unlikely to be a smooth transition.

Among the risks that could rattle bond markets is the unwinding of major central banks’ bond-buying programs, which could raise volatility, particularly at the longer end of the yield curve, by reducing liquidity and increasing the term premium demanded by investors. (The term premium is the additional yield required to compensate investors for the added risk of interest rate changes over a bond’s lifetime.)

Even though we expect major central banks to start gradually cutting rates from the middle of next year, short- and long-term rates will, in our view, settle at higher levels than we’ve become accustomed to in the past decade. While this will limit the potential gains from bond price increases, we believe the persistence of higher yields – a strong predictor of long-term bond returns – will ultimately benefit disciplined investors over the long run.

The bottom line

For bond investors, timing potential shifts in bond markets with asset allocation decisions is extremely challenging. It’s far better to focus on what investors can control – such as calibrating the duration of their bond portfolios to match their time horizons, which can help optimise investment outcomes while reducing exposure to interest rate and reinvestment risk.

The transition to a higher-for-longer rate environment has not been easy over the last few years. The good news is we’re nearing the end of this structural shift; which should ultimately provide a more solid foundation for delivering long-term bond returns.

The bottom line: Rather than a bane, the rise in interest rates is the single best development for investors in 20 years.

Read the full report to find out how our long-term asset return expectations have changed, including for bond portfolios.

Watch the Vanguard economic and market outlook for 2024 webinar for further insights, including a Q&A with Vanguard economists.

1 Source: Vanguard calculations based on data from Refinitiv. 10-year annualised total returns of the Bloomberg Global Aggregate Bond Index (EUR hedged) from 31 a 2007 to 31 December 2017 have been 3.9%, while yields on US 10-year government bonds at the start of that period were at 4.0%. After 2008, yields on 10-year government bonds for the US remained below 4% until the start of 2022. Details of our forecasted returns can be found in Vanguard’s Economic & Market Outlook 2024.

2 Hypothetical portfolio of bonds is represented by the Bloomberg Global Aggregate Bond Index (EUR hedged).

3 Based on the VCMM 10-year annualised nominal return forecasts as at 30 September 2023 and as at 31 December 2021 for euro area and global ex-euro area bonds (hedged) and global equities. Euro area bonds are represented by the Bloomberg Euro-Aggregate Bond Index, global ex-euro area bonds (hedged) are represented by the Bloomberg Global Aggregate Bond Index (EUR hedged) and global equities are represented by the MSCI AC World Total Return Index.

IMPORTANT: The projections or other information generated by the Vanguard Capital Markets Model® regarding the likelihood of various investment outcomes are hypothetical in nature, do not reflect actual investment results, and are not guarantees of future results. VCMM results will vary with each use and over time. The VCMM projections are based on a statistical analysis of historical data. Future returns may behave differently from the historical patterns captured in the VCMM. More important, the VCMM may be underestimating extreme negative scenarios unobserved in the historical period on which the model estimation is based.

The Vanguard Capital Markets Model® is a proprietary financial simulation tool developed and maintained by Vanguard’s primary investment research and advice teams. The model forecasts distributions of future returns for a wide array of broad asset classes. Those asset classes include US and international equity markets, several maturities of the U.S. Treasury and corporate fixed income markets, international fixed income markets, US money markets, commodities, and certain alternative investment strategies. The theoretical and empirical foundation for the Vanguard Capital Markets Model is that the returns of various asset classes reflect the compensation investors require for bearing different types of systematic risk (beta). At the core of the model are estimates of the dynamic statistical relationship between risk factors and asset returns, obtained from statistical analysis based on available monthly financial and economic data from as early as 1960. Using a system of estimated equations, the model then applies a Monte Carlo simulation method to project the estimated interrelationships among risk factors and asset classes as well as uncertainty and randomness over time. The model generates a large set of simulated outcomes for each asset class over several time horizons. Forecasts are obtained by computing measures of central tendency in these simulations. Results produced by the tool will vary with each use and over time.

Investment risk information

The value of investments, and the income from them, may fall or rise and investors may get back less than they invested.

Past performance is not a reliable indicator of future results.

Any projections should be regarded as hypothetical in nature and do not reflect or guarantee future results.

Some funds invest in emerging markets which can be more volatile than more established markets. As a result the value of your investment may rise or fall.

Funds investing in fixed interest securities carry the risk of default on repayment and erosion of the capital value of your investment and the level of income may fluctuate. Movements in interest rates are likely to affect the capital value of fixed interest securities. Corporate bonds may provide higher yields but as such may carry greater credit risk increasing the risk of default on repayment and erosion of the capital value of your investment.

The level of income may fluctuate and movements in interest rates are likely to affect the capital value of bonds.

Important information

For professional investors only (as defined under the MiFID II Directive) investing for their own account (including management companies (fund of funds) and professional clients investing on behalf of their discretionary clients). In Switzerland for professional investors only. Not to be distributed to the public.

The information contained herein is not to be regarded as an offer to buy or sell or the solicitation of any offer to buy or sell securities in any jurisdiction where such an offer or solicitation is against the law, or to anyone to whom it is unlawful to make such an offer or solicitation, or if the person making the offer or solicitation is not qualified to do so. The information does not constitute legal, tax, or investment advice. You must not, therefore, rely on the content of this document when making any investment decisions.

The information contained herein is for educational purposes only and is not a recommendation or solicitation to buy or sell investments.

Issued in EEA by Vanguard Group (Ireland) Limited which is regulated in Ireland by the Central Bank of Ireland.

Issued in Switzerland by Vanguard Investments Switzerland GmbH.

Issued by Vanguard Asset Management, Limited which is authorised and regulated in the UK by the Financial Conduct Authority.

© 2024 Vanguard Group (Ireland) Limited. All rights reserved.

© 2024 Vanguard Investments Switzerland GmbH. All rights reserved.

© 2024 Vanguard Asset Management, Limited. All rights reserved.