By Andrew Patterson, senior international economist, Vanguard.

- Global economic growth will likely stay positive this year but some economies are flirting with recession.

- We have increased our inflation forecasts and expect interest rates to rise higher and sooner than expected.

- With lower current equity valuations and higher interest rates, our model suggests higher expected long-term returns for most global markets.

A lot has changed since Vanguard published its economic and market outlook for 2022. At the start of the year, we expected global economies to continue to recover from the effects of the Covid-19 pandemic but at a more modest pace than in 2021. While this still holds true, the pace of change in the economic fundamentals – including inflation, growth and monetary policy – has failed to live up to expectations.

Labour-market and supply-chain constraints were already fuelling inflation before the year began but Russia’s invasion of Ukraine and China’s zero-Covid policies have exacerbated the situation. Central banks have been forced to play catch-up in the fight against inflation, ratcheting up interest rates more rapidly and possibly higher than previously expected. But those actions risk cooling economies to the point that they enter recession.

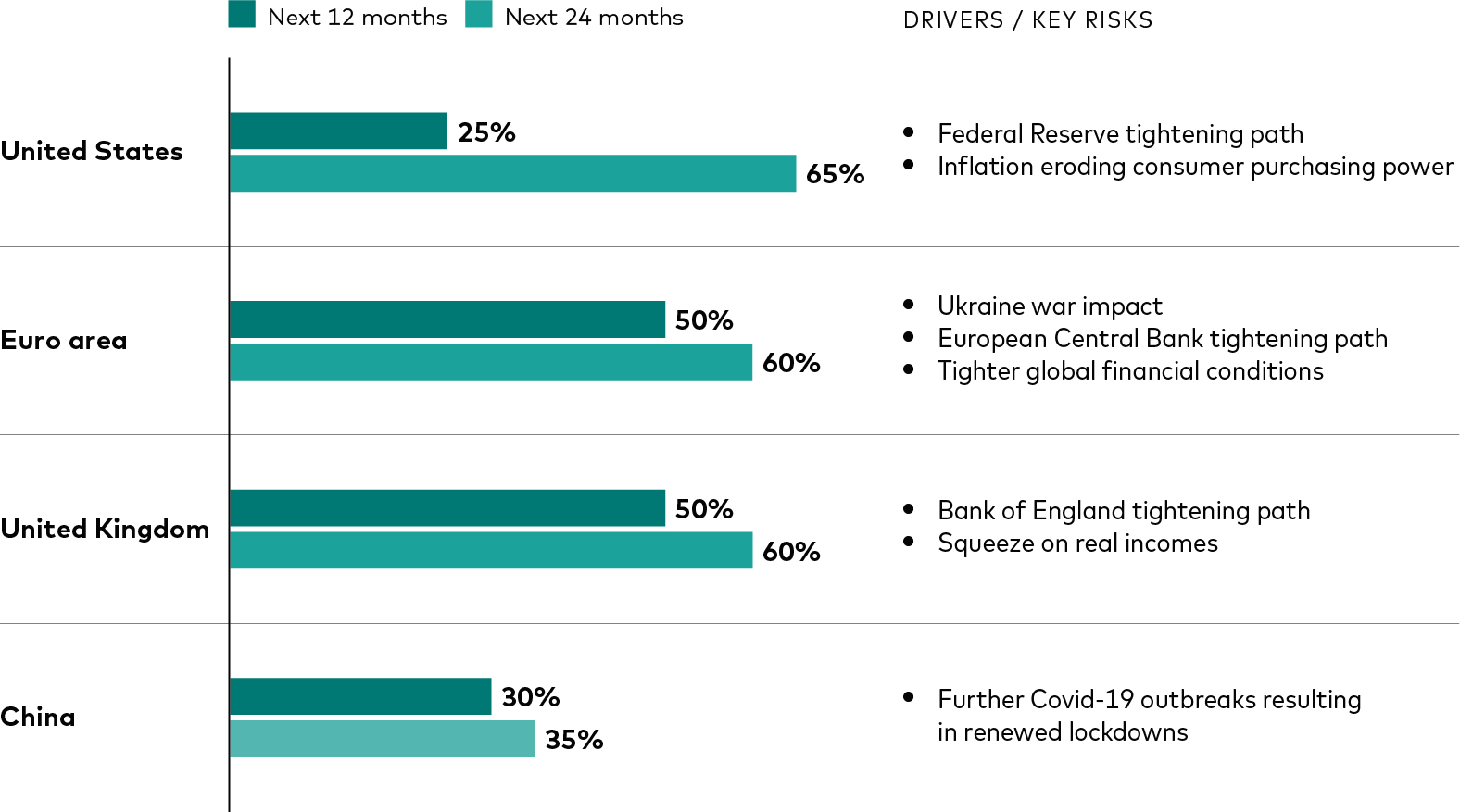

Global economic growth will likely stay positive this year but some economies are flirting with recession – if not this year, then in 2023.

Recession probabilities for select regions

Source: Vanguard forecasts as of 7 July 2022.

Compared with the start of the year, Vanguard has downgraded its 2022 GDP growth forecasts for all the major regions. We’ve also increased our inflation forecasts and expect interest rates to head even higher and sooner.

Vanguard’s forecasts for year-end 2022

| |

Economic growth |

Headline inflation |

Monetary policy |

Unemployment rate |

| United states |

c.1.5% |

7%-7.5% |

3.25%-3.75% |

3%-3.5% |

| Euro area |

2%-3% |

c.8%-8.5% |

0.5%-0.75% |

c.7% |

| United Kingdom |

3.5%-4% |

c.10% |

2.25%-2.5% |

c.4% |

| China |

c.3% |

< 2.5% |

2.75% |

c.5.5% |

Notes: Forecasts evolve with new data and our views will inevitably change. ‘Economic growth’ is the change in annualised GDP year over year. Headline inflation is the consumer price index, which includes the volatile food and energy sectors. ‘Interest rates’ is our year-end projection for the relevant central bank’s short-term interest rate target.

Source: Vanguard forecasts as at 7 July 2022.

Inflation, policy elevate the risk of recession

In the United States, inflation has reached 40-year highs, eroding consumers’ purchasing power and driving the Federal Reserve to aggressively raise interest rates. We expect the equivalent of 12 to 14 quarter-percentage-point hikes for the full year, with the target federal funds rates landing in the 3.25%-3.75% range by year-end. We also expect a peak rate1 of at least 4% in 2023 – higher than what we consider to be the neutral rate2 (2.5%) and above what’s currently priced into the market.

We have downgraded expected US GDP growth from about 3.5% at the start of the year to about 1.5%. The factors that led to our downgrade will likely continue through 2022 – namely, tightening financial conditions, wages not keeping up with inflation and lack of demand for US exports.

Labour market trends are likely to keep downward pressure on the unemployment rate through to the end of the year, though increases in 2023 are likely as the impact of tighter Fed policy and slowing demand is felt. We assess the probability of recession at about 25% over the next 12 months and 65% over 24 months.

We believe that a period of high inflation and stagnating growth is more likely than an economic “soft landing” in which growth and unemployment rates stay around or above longer-term equilibrium levels (about 2% for growth and 4% for unemployment).

Euro area and UK

In the euro area, inflation driven by high energy prices may climb to near 9% in the third quarter. Inflation has become widespread, spurring the European Central Bank into what it expects will be a “sustained path” of interest rate increases.

In September, policy rates will likely be out of negative territory for the first time in a decade.

We expect euro-area economic growth to come in at about 2.5% to 3% for the full year. However, Europe’s dependence on Russian natural gas and the challenges of managing monetary policy for 19 countries put the euro area at a higher risk of recession than the United States in the next 12 months. A complete cut-off from Russian gas would likely lead to rationing and recession.

In the United Kingdom, similarly, energy prices will likely drive the headline inflation rate to roughly 10% late in the year. We expect the Bank of England to raise the bank rate by an additional 1.25 percentage points, in total, over the next 12 months to reach our estimate of a 2.5% neutral rate2. The central bank has also signalled it is prepared to raise its policy rates by more than 0.25 percentage points at a time, depending on the economic and inflation outlook.

Even with rising inflation and a slowing economy, the labour market will likely stay strong, given record job vacancies and unemployment near a 50-year low. But a drop in real wages, combined with diminishing consumer and business confidence and tighter financial conditions, could push the UK into recession.

Vanguard sees the probability of UK recession at about 50% over the next 12 months. For 2022, we’ve downgraded our 5.5% forecast at the start of the year to 3.5% to 4%. Further out, the pending leadership change in the UK may bring some policy uncertainty.

China and emerging markets

China will fall far short of policymakers’ growth target of about 5.5%, given that it’s a challenge to achieve all three of their goals: the growth target, financial stability and a zero-Covid policy.

We believe that the country’s actual 2022 GDP growth rate will be just above 3%, far below China’s pace for many years. Given its zero-Covid approach, additional outbreaks resulting in renewed lockdowns could further detract from growth.

We also recently downgraded our forecast for full-year 2022 growth in emerging markets, from about 5.5% at the start of the year to about 3%. Emerging markets continue to face headwinds from slowing growth in the US, euro area and China, as well as from central bank policy tightening in developed markets and domestic and global inflation. Although higher commodities prices do benefit some emerging economies, they’re negative as a whole.

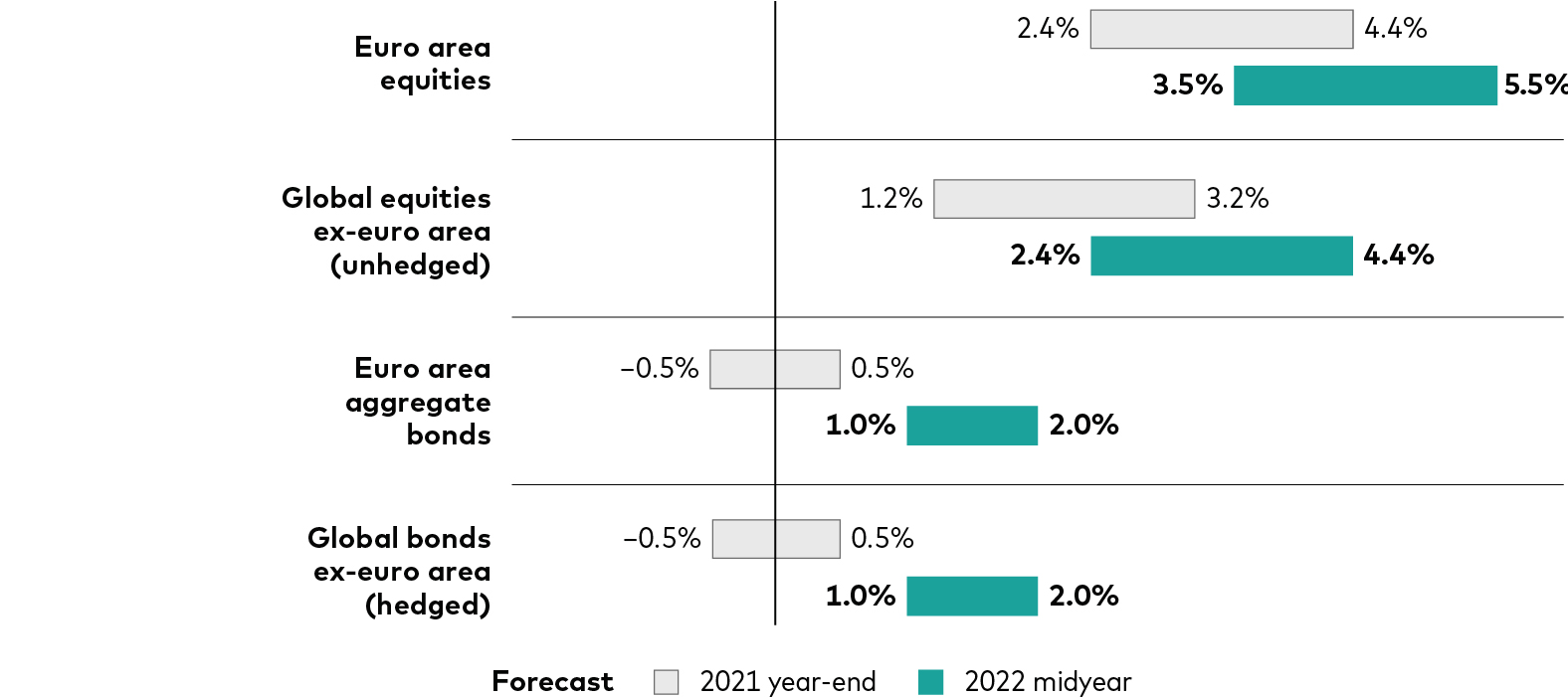

Expected 10-year asset class returns have risen

Stock and bond markets have been hit hard so far in 2022. But there is an upside to falling markets: Because of lower current equity valuations and higher interest rates, the latest running of our proprietary financial model, the Vanguard Capital Markets Model (VCCM)*, suggests higher expected long-term returns for global markets than at the start of the year.

Our 10-year annualised return forecasts for most equity markets are largely 1 percentage point higher than at the end of 2021, although slightly lower for the domestic UK market where our projections were already more elevated. Our bond return forecasts are also about 1.5 percentage points higher. Rising yields may detract from current bond prices but that means higher returns in the future as interest payments are reinvested in higher-interest bonds.

Global stock and bond market outlook

*IMPORTANT: The projections and other information generated by the VCMM regarding the likelihood of various investment outcomes are hypothetical in nature, do not reflect actual investment results, and are not guarantees of future results. Distribution of return outcomes from VCMM are derived from 10,000 simulations for each modelled asset class. Simulations as at 31 May 2022 and 31 December 2021. Results from the model may vary with each use and over time. For more information, please see the ‘Investment risk information’ section below.

Source: Vanguard. Notes: The figures are based on a 1-point range around the 50th percentile of the distribution of return outcomes for equities and a 0.5-point range around the 50th percentile for bonds. Indices used in VCCM simulations: for euro-area shares, the MSCI European Economic and Monetary Union (EMU) Index; for global ex-euro-area shares, the MSCI AC World ex EMU Index; for euro-area aggregate bonds, the Bloomberg Euro-Aggregate Bond Index; and for global ex-euro-area bonds, the Bloomberg Global Aggregate ex Euro Index. Returns are calculated in EUR and include the reinvestment of income.

1 Also known as the ‘terminal’ rate, this denotes the point at which a rate-hiking cycle is expected to end.

2 The neutral rate is the theoretical rate at which monetary policy is deemed to neither stimulate nor restrict an economy.