- Multi-asset investing involves diversifying investments across various assets with different risk and return correlations to reduce overall risk.

- Benefits of using multi-asset solutions including cost efficiency, time savings for financial professionals and peace of mind for investors.

- By leveraging multi-asset solutions, financial advisers can provide clients with diversified, low-cost portfolios and focus on delivering value through other advisory services.

Investing entails a level of risk. To help mitigate this, many investors seek to diversify their investments by spreading their money across different types of assets with low and negative return correlations, meaning returns from those assets tend to move in different directions relative to each other. This principle of portfolio diversification is the foundation of an effective multi-asset investment strategy.

Traditionally, multi-asset strategies have leaned on the long-term negative return correlation between global equity and bond markets, with the value of the bond component tending to rise when stock markets fall sharply or for a sustained period of time. The key benefit of this approach is that portfolio returns are smoothed over the long term with stock markets driving the majority of returns and bonds acting more as a ballast to stock market volatility. Well-diversified multi-asset portfolios are still susceptible to risk, but broad diversification across global equity and bond markets can help minimise that risk over the long-term.

Investors can build their own multi-asset portfolios or invest in a pre-packaged multi-asset fund or exchange-traded fund (ETF), constructed and managed by an investment company on their behalf.

What is a multi-asset fund?

A multi-asset solution is a single fund or ETF—like those which make up Vanguard’s LifeStrategy ETF range—that combines different types of investments. Traditionally, multi-asset solutions have combined investments in equities and bonds, with the exact blend of the two asset classes in the portfolio depending on the specific strategy. Strategies that invest more in stock markets have typically delivered greater returns over the long term, but at the expense of greater short-term volatility. Different mixes of equities and bonds cater for different investor preferences and goals, including variations in attitudes towards risk and time horizons.

Some multi-asset portfolios invest directly in a blend of individual equities and bonds, while others invest in other funds and ETFs that in turn invest in equities and bonds. The latter are known as funds of funds. These blended funds can give investors access to hundreds or even thousands of equities and bonds in a single investment. This means they can spread investors’ capital across a wide range of securities to achieve a high level of diversification.

Now we’ve established the definition of a multi-asset fund, let’s explore the key benefits for investors of using a single multi-asset ETF.

Why investors choose a multi-asset solution

1. Investment expertise

Building globally diversified portfolios is arguably the most important part of the investment process. Without the resources and scale of a global investment manager, it can be easy to miss overlapping investments that can skew a portfolio’s exposure to certain regions, sectors or even individual companies.

By investing in a pre-packaged multi-asset solution, investors can lean on a wealth of experience and expertise to invest in highly diversified portfolios that minimise biases and inefficiencies.

2. All-weather portfolios

Well-constructed, globally diversified multi-asset portfolios are designed to deliver value to investors through various economic and market environments. That doesn’t mean investors will always get positive returns, but an appropriate allocation to global bonds and global equities (according to an investor’s goals and attitude towards risk) can smooth returns over the long-term relative to more concentrated investment strategies1.

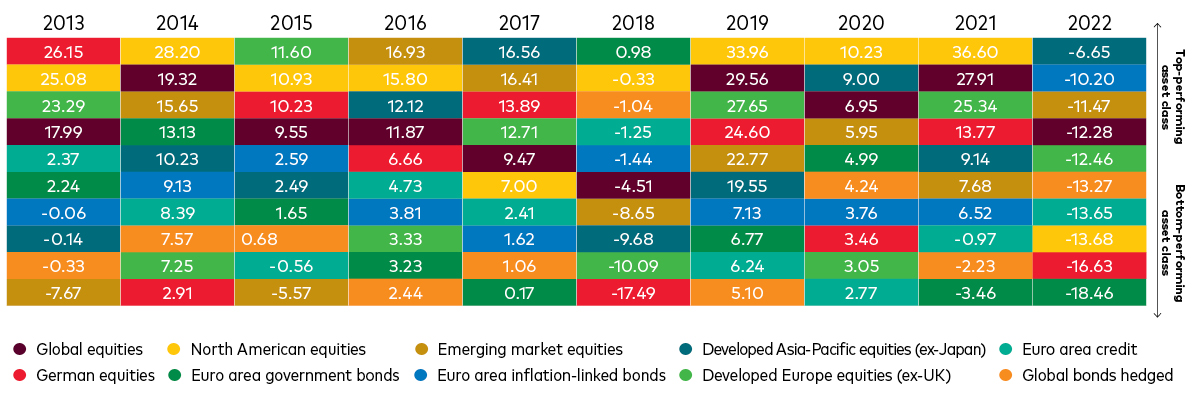

The chart below, which shows the annual return of different equities and bond market sub-asset classes over the past 10 years, illustrates why broad diversification across markets is a sensible approach for the vast majority of long-term investors. As the data highlight, it’s difficult to say exactly which investments within equities and bond markets will perform well from year to year.

Key bond and equity index returns (%), ranked by performance

Past performance is not a reliable indicator of future results.

Source: Vanguard calculations in EUR, based on data from Refinitiv. Data between 31 December 2012 and 31 December 2022. German equity is represented by the FTSE Germany Index, dev. Europe ex-UK equity by the FTSE Developed Europe ex-UK Index, dev. APAC ex-Japan equity by the FTSE Developed Asia Pacific Excluding Japan Index, North America equity by the FTSE North America Index, EM equity by the FTSE Emerging Index and global equity by the FTSE All World Index. Euro area inflation-linked bonds are represented by the Bloomberg Global Inflation-Linked: Eurozone - Euro Consumer Price Index, global bonds (hedged) by the Bloomberg Global Aggregate Bond Index Euro Hedged, Euro area government bonds by the Bloomberg Euro-Aggregate: Treasury Bond Index Euro area credit by the Bloomberg Euro-Aggregate: Corporates Bond Index. Returns do not take into account management fees and expenses, nor do they reflect the effect of taxes. Returns include the reinvestment of income and capital gains. Indices are unmanaged; therefore, direct investment is not possible.

By investing across global markets, pre-packaged multi-asset portfolios capture the returns from the best-performing investments in any given year and minimise the impact of the poorest-performing investments on total returns.

3. Cost efficiency

Building a globally diversified portfolio of equities and bonds can be costly. Our research has shown low-cost funds and ETFs have a higher probability of performing better than costlier ones2. By investing in a low-cost, well-diversified multi-asset solution, investors can attain a level of portfolio diversification that would be much more expensive to achieve by investing in individual funds themselves, given the costs involved.

For example, Vanguard’s LifeStrategy 60% Equity ETF , which consists of 60% equities and 40% bonds, provides exposure to global markets through up to 14 different underlying ETFs and more than 20,000 constituent securities. Investors only pay one fee, rather than the multiple fees that would be required to invest in all the underlying investments.

Not all multi-asset portfolios are created equal, however. Investors should consider whether they will be achieving a good level of diversification and that the ongoing costs are low before deciding to allocate investments into a multi-asset solution.

4. More time back

Multi-asset ETFs can free up time for advisers to focus on adding value through the range of adviser services beyond portfolio construction. Using an all-in-one investment solution means that advisers needn’t spend significant amounts of their time choosing individual funds or managing client portfolios – or undertaking the administrative tasks that go with it.

Whether it’s behavioural coaching to improve client outcomes and strengthen relationships or focusing on more specific client needs like estate planning, advisers who use appropriate multi-asset solutions get the value of having more time back to dedicate to their clients’ financial planning needs.

For example, depending on the asset allocation strategy, multi-asset managers will typically rebalance client portfolios to either maintain a pre-determined mix of equities and bonds or to one that is commensurate with the objective of the fund, for example achieving a certain level of return.

Investing in multi-asset ETFs that are rebalanced by the investment manager means there is no need for advisers to manually rebalance portfolios. By taking on the rebalancing responsibility, investment managers relieve advisers from the burden and associated complexity that can come from gaining permission from each and every investor before changes can be made. As well as preserving a portfolio’s risk profile, the process ensures both advisers and clients are clear on how the portfolio is invested at any time.

Another time-saving factor to consider is the simplicity of choice when picking the appropriate multi-asset solution. Most multi-asset managers offer a range of different portfolios with different levels of potential risk and return, usually based on their equity-to-bond ratios. Advisers simply need to pick the portfolio that best reflects the client’s goals and attitude towards risk.

5. Peace of mind

By using a multi-asset solution constructed and overseen by an investment manager with global scale and a large team with deep expertise—as well as a strong track record in delivering effective multi-asset strategies—investors benefit from the peace of mind that comes from knowing their investments are in capable hands. That doesn’t eliminate the risks associated with investing in global equity and bond markets as the value of investments, and income from them, may fall or rise and no investor is guaranteed to make a profit.

The risks associated with investing are part of the reason why multi-asset managers often employ large teams of investment professionals dedicated to the ongoing management of multi-asset portfolios. By choosing a multi-asset ETF that benefits from a depth of expertise, advisers and clients are provided a layer of comfort amid the complexities and risks of participating in investment markets.

6. Support

Effective communication also promotes trust among clients. This is why some multi-asset managers regularly provide advisers with materials to aid client conversations by keeping them informed and helping to instil confidence.

For example, quarterly fund performance updates and regular macroeconomic insights can help advisers provide clarity and context for clients, while behavioural coaching tips and aids can support advisers in having effective conversations with clients during difficult and even sanguine market conditions. In some cases, multi-asset managers offer practice management insights for advisers to help strengthen their businesses. All-in-all, advisers can leverage the insights and thought leadership provided by multi-asset managers to strengthen their business and deliver better outcomes for clients.

Delivering value to clients

In today’s fast-paced market and economic environment, more and more advisers are outsourcing their investment proposition and entrusting their clients’ capital to a robust multi-asset solution.

In doing so, advisers can leverage the portfolio construction expertise of multi-asset managers to provide clients with an all-weather portfolio at a low cost without having to spend a significant amount of time on building and maintaining the portfolio.

At the same time, advisers can get more time back by using an all-in-one multi-asset solution to spend on higher-value tasks and achieve the peace of mind that comes from the knowledge that client capital is in reliable hands, while using the materials and guidance made available by their chosen multi-asset manager to deliver more value to clients.

1 Source: Vanguard Research: “How to increase the odds of owning the few stocks that drive returns”, February 2019, C. Tidmore, F. M. Kinniry, G. Renzi-Ricci; E. Cilla. Data between 1 January 1987 to 31 December 2017. Based on quarterly Russell 3000 Index constituents’ return data from Thomson Reuters Market QA.

2 Source: Morningstar and Vanguard. In a 2010 analysis across universe of funds, researchers found that, regardless of fund type, low expense ratios were the best predictors of future relative outperformance (Kinnel, 2010).

Investment risk information

The value of investments, and the income from them, may fall or rise and investors may get back less than they invested.

Some funds invest in emerging markets which can be more volatile than more established markets. As a result the value of your investment may rise or fall.Investments in smaller companies may be more volatile than investments in well-established blue chip companies.

ETF shares can be bought or sold only through a broker. Investing in ETFs entails stockbroker commission and a bid- offer spread which should be considered fully before investing.

Funds investing in fixed interest securities carry the risk of default on repayment and erosion of the capital value of your investment and the level of income may fluctuate. Movements in interest rates are likely to affect the capital value of fixed interest securities. Corporate bonds may provide higher yields but as such may carry greater credit risk increasing the risk of default on repayment and erosion of the capital value of your investment. The level of income may fluctuate and movements in interest rates are likely to affect the capital value of bonds.

The Funds may use derivatives in order to reduce risk or cost and/or generate extra income or growth. The use of derivatives could increase or reduce exposure to underlying assets and result in greater fluctuations of the Fund's net asset value. A derivative is a financial contract whose value is based on the value of a financial asset (such as a share, bond, or currency) or a market index.

Some funds invest in securities which are denominated in different currencies. Movements in currency exchange rates can affect the return of investments.

For further information on risks please see the “Risk Factors” section of the prospectus on our website.

Important information

This is a marketing communication.

For professional investors only (as defined under the MiFID II Directive) investing for their own account (including management companies (fund of funds) and professional clients investing on behalf of their discretionary clients).

For further information on the fund's investment policies and risks, please refer to the prospectus of the UCITS and to the KIID (for UK, Channel Islands, Isle of Man investors) and to the KID (for European investors) before making any final investment decisions. The KIID and KID for this fund are available in local languages, alongside the prospectus via Vanguard’s website.

The information contained herein is not to be regarded as an offer to buy or sell or the solicitation of any offer to buy or sell securities in any jurisdiction where such an offer or solicitation is against the law, or to anyone to whom it is unlawful to make such an offer or solicitation, or if the person making the offer or solicitation is not qualified to do so. The information is general in nature and does not constitute legal, tax, or investment advice.

Potential investors are urged to consult their professional advisers on the implications of making an investment in, holding or disposing of shares and /or units of, and the receipt of distribution from any investment.

Vanguard Funds plc has been authorised by the Central Bank of Ireland as a UCITS and has been registered for public distribution in certain EEA countries and the UK. Prospective investors are referred to the Funds' prospectus for further information. Prospective investors are also urged to consult their own professional advisers on the implications of making an investment in, and holding or disposing shares of the Funds and the receipt of distributions with respect to such shares under the law of the countries in which they are liable to taxation.

The Manager of Vanguard Funds plc is Vanguard Group (Ireland) Limited. Vanguard Asset Management, Limited is a distributor for Vanguard Funds plc.

The Manager of the Ireland domiciled funds may determine to terminate any arrangements made for marketing the shares in one or more jurisdictions in accordance with the UCITS Directive, as may be amended from time-to-time.

The Indicative Net Asset Value (“iNAV”) for Vanguard’s ETFs is published on Bloomberg or Reuters. Refer to the Portfolio Holdings Policy.

For investors in Ireland domiciled funds, a summary of investor rights. is available in English, German, French, Spanish, Dutch and Italian.

London Stock Exchange Group companies include FTSE International Limited ("FTSE"), Frank Russell Company ("Russell"), MTS Next Limited ("MTS"), and FTSE TMX Global Debt Capital Markets Inc. ("FTSE TMX"). All rights reserved. "FTSE®", "Russell®", "MTS®", "FTSE TMX®" and "FTSE Russell" and other service marks and trademarks related to the FTSE or Russell indexes are trademarks of the London Stock Exchange Group companies and are used by FTSE, MTS, FTSE TMX and Russell under licence. All information is provided for information purposes only. No responsibility or liability can be accepted by the London Stock Exchange Group companies nor its licensors for any errors or for any loss from use of this publication. Neither the London Stock Exchange Group companies nor any of its licensors make any claim, prediction, warranty or representation whatsoever, expressly or impliedly, either as to the results to be obtained from the use of the FTSE or Russell indexes or the fitness or suitability of the indexes for any particular purpose to which they might be put.

For Dutch investors only: The fund(s) referred to herein are listed in the AFM register as defined in section 1:107 Dutch Financial Supervision Act (Wet op het financieel toezicht).For details of the Risk indicator for each fund listed, please see the fact sheet(s) which are available from Vanguard via our website.

Issued in EEA by Vanguard Group (Ireland) Limited which is regulated in Ireland by the Central Bank of Ireland.

© 2024 Vanguard Group (Ireland) Limited. All rights reserved.